Here's what most people never realize: almost everything on your monthly bill is negotiable. Not in a sketchy, haggling-at-a-flea-market way — in a completely legitimate, the-company-would-rather-keep-you-than-lose-you way. Businesses build retention budgets specifically because acquiring a new customer costs five to seven times more than keeping an existing one, according to research from Bain & Company. That budget exists. That money is sitting there. And the only thing standing between you and it is a phone call, a little preparation, and the willingness to ask.

This isn't about becoming a coupon-clipping extremist or living like you're on a perpetual spending freeze. It's about being intentional — a core Harmony Hub value — with where your money actually goes, so more of it can flow toward the things that genuinely matter to you. Let's get into it.

1. Know Your Numbers First

Before you call a single company, do the one thing most people skip: sit down with three months of bank or credit card statements and build a complete picture of your recurring expenses. Every subscription, every auto-pay, every "I forgot that was still on" charge. Write them all down in one place — the service name, the amount, and when you last actually used it. This exercise is equal parts financial hygiene and mild horror show.

The average American household spends over $219 per month on subscription services alone, according to a 2022 C+R Research study — and nearly 42% of respondents had forgotten about at least one active subscription they were still being charged for. That's not a budgeting problem. That's a visibility problem. You cannot negotiate what you cannot see, and you cannot cut what you don't know exists. Spend thirty quiet minutes with your statements before anything else. Think of it as a financial inventory — the kind of decluttering that Marie Kondo would absolutely approve of.

2. The Loyalty Paradox — Being a Good Customer Costs You

Here's a maddening truth about the American billing system: companies routinely offer their best rates to new customers while quietly charging loyal, long-term customers significantly more for the exact same service. Your reward for faithfully paying your internet bill for five years is often a rate that's 30–50% higher than what a brand-new customer would pay today. This isn't an accident. It's a business model.

The moment you realize this, something shifts. You stop feeling like you're asking for a favor when you call to negotiate — because you're not. You're simply pointing out an imbalance and asking the company to correct it. Frame the conversation accordingly. "I've been a customer for six years and I just noticed new customers are being offered this same plan for $40 less. I'd like that rate, please." Calm, factual, direct. No drama required. That framing alone closes more deals than any amount of begging or bluffing.

3. The Magic of the Retention Department

Most people who call to negotiate a bill talk to a frontline customer service representative — and then hang up disappointed when they're told "there's nothing we can do." Here is the single most valuable phrase in bill negotiation: "Can you transfer me to your retention department?" or "I'd like to speak with someone in customer loyalty, please."

Retention departments exist for one reason: to keep customers from canceling. They have access to promotional rates, credits, package adjustments, and discounts that standard customer service reps simply cannot offer. They are the people with actual authority to give you something. Getting past the front line isn't rude — it's smart. If the first rep says there's no retention department (which is almost never true), politely say you'd like to discuss canceling your account. That phrase alone tends to unlock a transfer faster than anything else.

4. Do Your Competitor Homework

Walking into a negotiation without a competing offer is like playing poker without looking at your cards. Before you call your internet, cable, phone, or insurance provider, spend ten minutes researching what competitors in your area are currently offering. Screenshot it. Write down the price, the speed or coverage, and the terms. This isn't about actually switching — it's about having a real, specific alternative that changes the entire dynamic of the conversation.

"I've been looking at [Competitor X], who's offering the same speed for $35 less per month" is a fundamentally different conversation from "I think I'm paying too much." One is vague. One is a business decision waiting to happen. Most retention agents are trained to match or beat a documented competing offer — because a customer who leaves costs the company far more than a modest discount. Do the research. Bring the receipts. Feel the power of actually being prepared.

5. Attack Your Insurance Bills

Car insurance, renters insurance, homeowners insurance — these are among the most reliably negotiable bills most people have, and among the least frequently renegotiated. Rates shift constantly based on market conditions, your driving record, your credit score, and competitor pricing. If you haven't called your insurance provider in the last 12 months, there's a reasonable chance you're overpaying, and an even better chance that a competitor would happily take your business for less.

Call your current provider first and ask directly: "What discounts am I currently not receiving, and what would qualify me for a lower rate?" You'd be amazed what comes out of that question — safe driver discounts, bundling credits, paperless billing reductions, loyalty rates that weren't automatically applied. Then get two or three competitor quotes using aggregator tools like The Zebra or Policygenius. According to the Insurance Information Institute, the average driver who shops around saves between $300 and $500 per year just by switching providers. That's a car payment. That's a weekend trip. That's yours, if you ask.

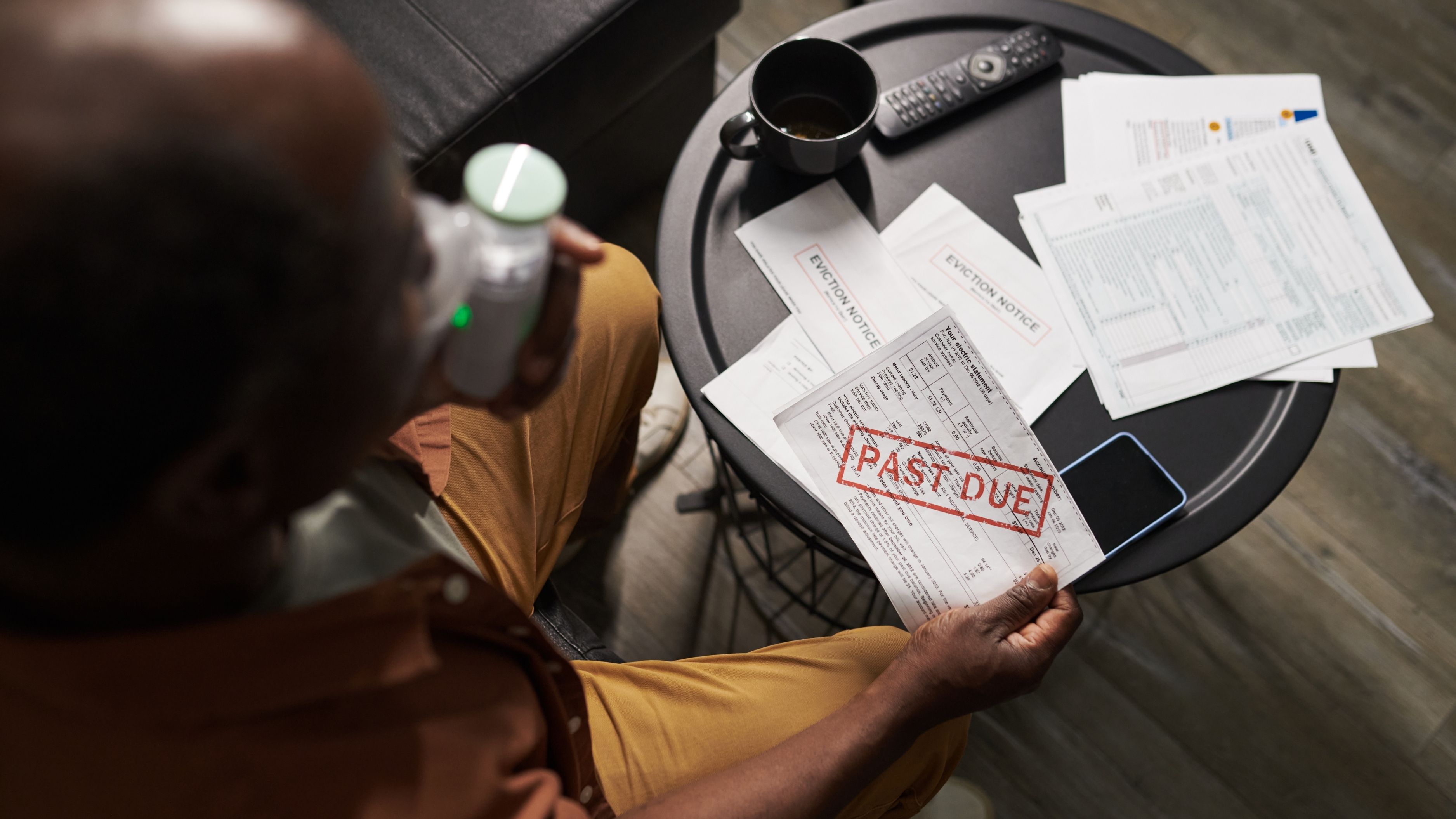

6. Medical Bills Are Almost Always Negotiable

This one surprises people most: medical bills — even large, frightening ones — are frequently negotiable, and hospitals and medical providers have entire billing departments set up to facilitate exactly that. Most people pay whatever the bill says because it looks official and intimidating. But that number is typically a starting point, not a final offer.

Start by requesting an itemized bill and checking it carefully for errors — studies suggest that up to 80% of medical bills contain mistakes, according to the Medical Billing Advocates of America. Then call the billing department and ask whether they offer a prompt-pay discount (paying in full upfront often earns 10–30% off), a hardship reduction, or a payment plan without interest. Non-profit hospitals are legally required under the Affordable Care Act to have financial assistance programs for qualifying patients — programs that often go entirely unclaimed because no one knows to ask. Ask. Always ask.

7. Credit Card Interest Rates — Just Call

Of all the negotiating wins available to the average consumer, this one might be the most overlooked and the most impactful. Your credit card's APR is not fixed by the laws of nature. It is a number that your issuer set, and it is a number your issuer can change — particularly if you have a solid payment history and have been a cardholder for a meaningful amount of time.

A survey by CreditCards.com found that 69% of cardholders who called and asked for a lower interest rate received one — often within a single phone call. The script is almost embarrassingly simple: "I've been a customer for [X] years, I've always paid on time, and I'd like to request a lower APR on my account." That's it. You don't need a compelling story or a hardship narrative. You just need to ask. If you're carrying a balance, even a three to five percentage point reduction can save hundreds of dollars annually. The call takes eight minutes. Do the math on your own hourly rate.

8. Utilities — More Flexible Than You Think

Electric, gas, and water bills feel fixed — like gravity, they just are what they are. But most utility companies offer programs, plans, and adjustments that dramatically reduce monthly costs for customers who know to look. Budget billing plans smooth out seasonal spikes by averaging your annual usage into consistent monthly payments. Time-of-use pricing plans reward customers who shift energy consumption to off-peak hours. Low-income assistance programs (LIHEAP, for example) provide direct bill relief for qualifying households.

Beyond the programs, many utilities offer free home energy audits that identify specific inefficiencies in your home — the drafty window, the ancient water heater, the refrigerator running five degrees colder than necessary — and provide rebates for making upgrades. Call your utility provider and ask what programs you currently qualify for. Ask what their most cost-effective billing plan is for your usage pattern. These conversations take fifteen minutes and routinely uncover savings that have been silently available for years.

9. The Subscription Audit (a.k.a. The Purge)

Go back to that list from tip one. Now ask, with genuine honesty, which of those subscriptions have you used more than twice in the last 60 days. Not "might use someday." Not "used once and meant to go back." Actually used, regularly, in a way that adds real value to your life. For the ones that pass that test — keep them, and perhaps negotiate the rate. For the rest — cancel them without ceremony.

Streaming services in particular have multiplied like houseplants in a wellness blogger's apartment — and most households are paying for three to five they barely use. Most platforms now offer cheaper ad-supported tiers that deliver identical content at 30–50% lower cost. Rotating subscriptions — subscribing to one service, bingeing what you want over a month, then canceling and moving to the next — is a completely legitimate, increasingly popular strategy that costs a fraction of keeping everything active simultaneously. Your entertainment doesn't need to be unlimited. It just needs to be intentional.

10. Timing Is Everything

The best time to negotiate is not when your contract has just renewed, your rate has been locked in for another year, and the company has zero incentive to move. The best time is before a renewal, when you're still in the window of decision — or immediately after a rate increase notice arrives in your inbox. That notice isn't just bad news. It's leverage. It is the company voluntarily handing you a reason to call.

Set calendar reminders 30 days before each major service contract renews. Mark the date your promotional rate on any service is set to expire. Create a simple document with each service, its current rate, and its renewal date — and treat those dates like appointments. Intentional timing turns bill negotiation from a reactive scramble into a proactive, low-stress ritual. One afternoon per quarter, a handful of calls, and a potential savings of hundreds of dollars — that is not a bad return on an afternoon's attention.

11. Master the Art of the Graceful Goodbye

Sometimes the best negotiating tool is the genuine willingness to leave. Not a bluff, not a performance — but an actual, prepared readiness to cancel or switch if the company won't meet you reasonably. This changes the energy of a negotiation entirely, and companies can sense the difference between someone who is posturing and someone who has already looked up the competitor's onboarding process.

Before your call, know your walkaway number — the rate at which you'd genuinely be willing to stay — and the alternative you'd genuinely pursue if they don't meet it. When you reach that threshold in the conversation, say so clearly and calmly: "I appreciate your help, but if that's the best available, I'll need to go ahead and cancel." Then stop talking. Silence after that sentence is your most powerful tool. Retention agents are trained to work within the space of that pause. Let them fill it.

The Bigger Picture

Here's the thing about bill negotiation that nobody puts on a motivational poster: it's an act of self-respect. Every dollar you reclaim from a bill you were overpaying is a dollar that gets redirected toward something you actually chose — savings, experiences, rest, generosity. It's money voting for your actual life rather than a corporation's quarterly earnings report.

You don't have to do it all at once. Pick one bill this week. Make one call. Get one win under your belt — and feel that small, satisfying shift of realizing that the terms of your financial life are more flexible than they appeared. Your budget doesn't need to be perfect. It just needs to be more yours.

📚 Sources

Bain & Company. (2020). "Prescription for Cutting Costs: Loyal Relationships." Bain.com.

C+R Research. (2022). "Subscription Service Survey: Average Monthly Spend." CRResearch.com.

CreditCards.com. (2023). "Survey: 69% of Cardholders Who Ask for Lower APR Receive One." CreditCards.com.

Medical Billing Advocates of America. (2023). "Medical Billing Error Statistics." BillAdvocates.com.

Insurance Information Institute. (2023). "How to Save Money on Car Insurance." III.org.

U.S. Department of Health & Human Services. (2023). "Low Income Home Energy Assistance Program (LIHEAP)." HHS.gov.

Reichheld, F. F. (2001). Loyalty Rules! How Today's Leaders Build Lasting Relationships. Harvard Business Review Press.

🔍 Explore Related Topics